Materiality Assessment

LINK has been performing the materiality assessment since 2020. In 2023 it was for the first time based on the European Sustainability Reporting Standards (ESRS), as prescribed by the EU Corporate Sustainability Reporting Directive (CSRD). It has been reviewed annually, either in a complex, or simplified manner.

The Process

LINK’s materiality assessment process follows a double materiality principle, covering both impact and financial perspective. The top-bottom approach is applied, with an assessment performed at a group level, while engaging internal stakeholders from all geographic regions, in which LINK operates, as well as the ones relevant for various departments and for the Company as a whole. The process considers all LINK entities, as well as value chain related matters.

LINK’s materiality assessment process consists of the following phases and steps:

Phase 1: Preliminary assessment

Identification of stakeholder groups:

Identification of the affected stakeholders and users of sustainability statements.Description of ESG matters and their context to LINK:

Specification of LINK’s context to circa 90 ESG topics listed in the ESRS.Defining a short-list of potentially material ESG matters:

Identification of circa 30 ESG matters that may potentially be material in LINK’s specific context.

Phase 2: Defining impacts, risk and opportunities

Identification and description of impacts, risk, opportunities:

Specifying impacts, risks and opportunities (IROs) connected with the short-listed ESG matters that may be material to LINK’s own operations and its value chain in a short-, medium- and/or long- term.

Phase 3: Impact and financial assessment

Preparation of a template for collecting data from stakeholders:

Developing an extensive template covering short-listed ESG matters and corresponding IROs, together with a dedicated space for adding next entries.Stakeholders’ assessment, including:

(a) initial assessment – initial materiality assessment of the short-listed ESG matters;

(b) impact assessment – assessment of impacts related to the topics chosen during initial assessment;

(c) financial assessment – assessment of risks and opportunities related to the topics chosen during initial assessment.

Phase 4: Identifying results and their implications

Materiality matrix:

Extensive analyses of assessment data collected from stakeholders; calculation of impact and financial materiality; preparation of materiality matrix, specification of qualitative and quantitative thresholds for the identification of material matters.Identification of LINK’s material matters:

Choice of material matters based on the pre-defined criterions and adopted threshold.Identification of strategic implications of the materiality assessment:

Including results of the materiality assessment in LINK’s risk management framework and the annual review of LINK’s policies; identification of the scope of the sustainability reporting and its communication to the internal stakeholders within the scope of the project “LINK’s road to CSRD compliance”.

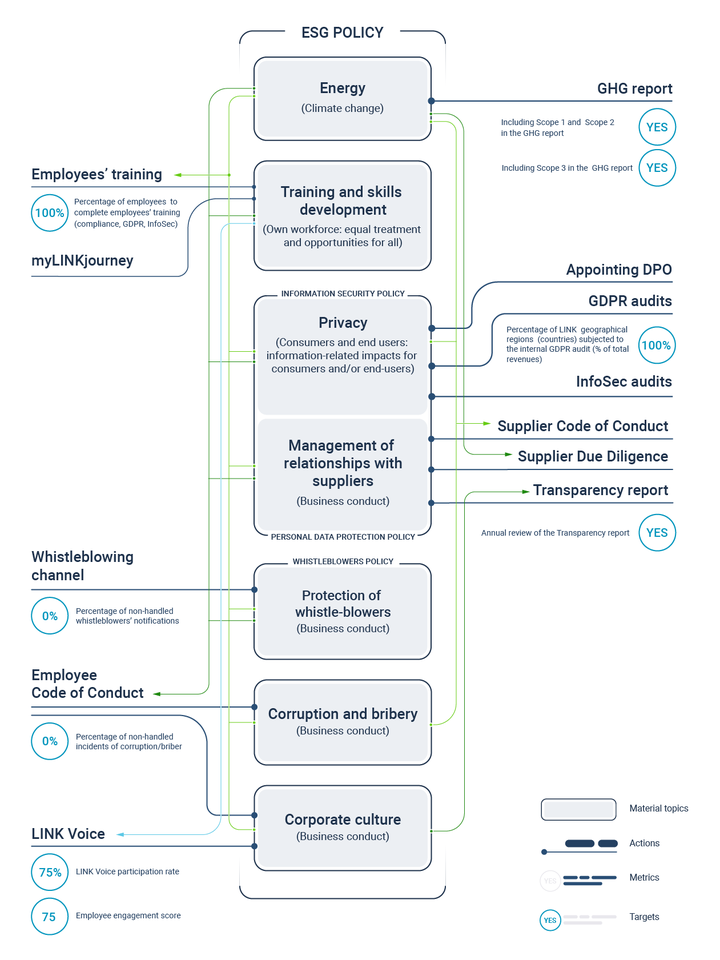

The Results

At present LINK identifies 8 material sustainability matters (material topics). All of them are taken into consideration during the annual review and update of LINK’s policies. In order to address each of the identified material matter, LINK takes or intends to take actions that will be assessed against the targets with the use of relevant metrics.

LINK’s material topics are the following:

1. Climate change mitigation

2. Energy

3. Training and skills development of own workforce

4. Privacy of consumers and end-users

5. Corporate culture

6. Protection of whistle-blowers

7. Management of relationships with suppliers

8. Corruption and bribery

LINK’s material topics, together with corresponding policies, actions, metrics and targets, are presented below: